Retirement Income Planning

We offer financial strategies that can protect your retirement portfolio and savings from recession, will boost buying power and protect against inflation, have ZERO net cost long term, and can be guaranteed to not lose principal. The proper use of structured income producing investments and assets are their own specialty and require strict adherence and continued compliance with many different specialized tax codes.

Customized retirement planning strategies are designed to maximize income and financial security while minimizing tax liabilities. Our approach includes structured financial models, tax-deferred and tax-free investment strategies, and estate preservation plans.

STRATEGIC TAX PLANNING

RMD SOLUTIONS

TAX DEFICIENCY & IRS REPRESENTATION

Are you a doctor, IT engineer or other high earning professional? Your Qualified 401 (k) has six or seven figures or even a few million. Great! If you have a lot of money in COMPANY STOCK or RSU’s or CASH saved in your 401(k) and are CONCERNED ABOUT THE TAX on your eventual REQUIRED MINIMUM DISTRIBUTIONS for whatever reason, or if your income also exceeds IRS income brackets to be eligible for a Roth or Mega Roth, we can completely solve or mitigate the RMD tax problem for you. COME TO ONE OF OUR FREE SEMINARS.

We also offer installment sales strategies and capital gains tax strategies for investments and business sales, and facilitate 1031 tax-deferred commercial property exchanges without the restraints of a 1031.

Call or email us for your complementary strategy appointment to review your personalized custom- crafted plan. We show you the math. Call us for an appointment, speak to us in person or on zoom.

TAX DEFICIENCY & IRS REPRESENTATION

Our firm provides IRS representation, tax resolution and mediation services, helping clients negotiate IRS Notices of Deficiency, Collection Due Process Hearings, Audits, IRS Form 5500 issues, Liens, Levies, Penalty and Interest Abatements, Innocent Spouse and Injured Spouse, and other complicated tax settlement agreements for tax debt relief. Dennis Noss is licensed with unlimted rights by the Treasury Department to practice all matters concerning taxation before the IRS.

Investment Portfolio Management

Cayman Capital is an independent financial management boutique and a securities licensed registered investment and tax advisory firm. Our firm offers many different customized strategies that are designed to protect your account from market loses due to volatility and adverse events with loss of principal protections. Cayman Capital structures individual investment portfolios using diversified asset classes, structured products and stock market participation.

When the stock market takes even a temporary dive of 35% you have to make 53% back to break even. 50% is 100% break even.

The majority of highly marketed Investment Firms like Fisher Investments, Fidelity Investments, JP Morgan etc. all have a similar public disclaimer that proclaims: “Consult your tax professional before investing in our recommendations.” Our firm does not need to state such a public disclaimer. Dennis Noss is an IRS Enrolled Agent and licensed stock market professional. His specialized expertise is understanding the complexities of combining income producing investments with safety strategies to protect from loss, while eliminating or minimizing the tax. He does not do tax returns. Your CPA or other licensed tax professional has the competent expertise for doing tax returns.

Our firm is also in partnership with Ni Advisors offering Private Placements, Preferred Offerings, Commercial REIT Investments, Leasehold Income, etc. EMAIL US TO REQUEST TO BE ON OUR EMAIL LIST FOR LATEST PROPOSALS & INVITATIONS. COME TO ONE OF OUR SEMINARS.

Beside personally designed strategies like the Flex Method, and other individually customized portfolios, we also represent Gradient Investments. Gradient Investments are Buffered Stock Market Indices. Although not individually customized, Buffered Stock Market Index Investments will also protect against market downturns, while maximizing returns. Please Click on: Buffered Investing. After reviewing the current Buffered Investment Offerings, Click on the CAYMAN LOGO seen at the Top to return to the CAYMAN CAPITAL Website.

For Asset Protected Savings Plans

These tax-advantaged strategies enhance individual supplemental income and retirement savings and investments for future income.

A customized overall financial and asset strategy is tailored to your risk tolerance, investment objectives and time horizon, and ever-evolving financial goals. We are also able to analyze multiple investment strategies tailored to your risk tolerance, time horizon, investment objectives and income needs.

We use prudent forecasts to illustrate how your income and asset portfolio balances will move overtime, and then compare what you have saved or invested, to what you have saved or invested with a recommended strategy. We show you the math.

The structured asset products we use are also used frequently by Estate Planning Lawyers and Tax Lawyers to maximize income and mitigate taxation for retirement, succession planning, and for business entity buy-sell agreements.

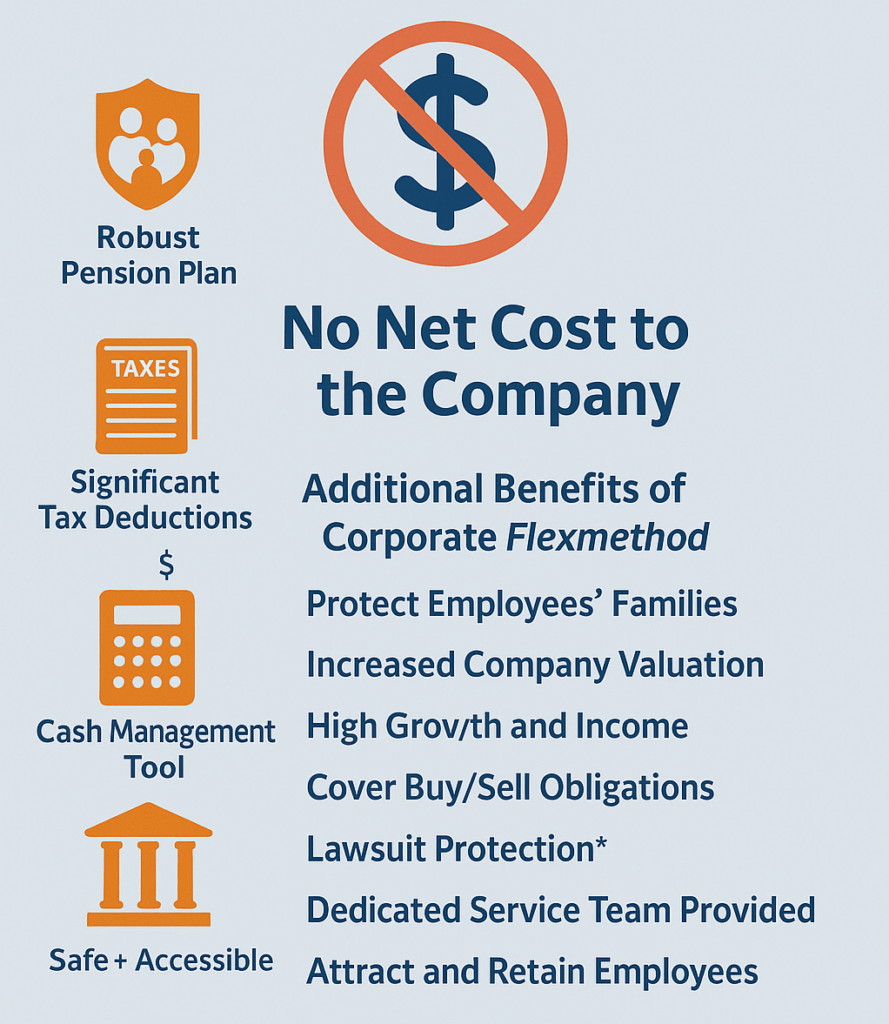

Business Tax Strategies

We provide tailored tax solutions for businesses, including retirement savings plans and employee retention strategies. We work directly with business owners to design planning strategies that will eliminate costs instead of taking deductions, will maximize revenue, and will mitigate or eliminate the tax for more income when it’s needed. We offer customized tax planning by recapturing taxes for individuals and business and offer compliance assistance.

Key Employee Retention Strategies

THE ADVANTAGES OF COMPANY OWNED LIFE INSURANCE (COLI) See Above Video

- The IRS recognizes company owned life insurance (COLI) under Internal Revenue Code Section 162.

- 70% of employees leave within 5 years. A Pulse survey found that 78% of today’s business leaders rate retention and recruitment as one of their top concerns.

- Replacement cost in the Tech industry is more than double that person’s annual salary.

- Company shows no debt on the Balance Sheet.

- The company determines the employee vesting period and policy terms for this benefit.

- There is no gifting required to transfer the ownership of the policy to the employee.

- There is no cost of insurance to the employer and the employer saves FICA expenses.

- The plan eliminates a company expense instead of taking a deduction thereby improving the Earnings Before Interest Taxes Depreciation Amortization (EBITDA)

- The company owns the policy as an asset until the policy transfers to the employee or can retain the policy as an asset if the employee leaves the company before becoming vested.